hi in this lecture and in the next one we’re going

to be talking about banking and payment security this is a really important issue for the security

engineer because an awful lot of the attacks that happen on systems are after the money and we

have to understand how things like online banking um and credit cards and even cryptocurrencies work

because these are the mechanisms for fraud and the targets for fraudsters so we already talked

a little bit about bank security in the first couple of lectures we looked at bulk compromise

how espionage agencies try and get hold of back information at scale in order to do

surveillance of target populations there’s also bulk compromised by crooks who for example

may try and get lots of personal information from one bank say from the register of anti-money

laundering information that people have given so they can use it to open accounts elsewhere and

there may be whistleblowers who are trying to tell journalists about bad things

being done by famous people now there are also more targeted attacks

where a journalist might be after information about a celebrity a rock star politician or

whatever and these are generally controlled by internal controls in the old days that meant

limiting information on customers to the branches where their accounts were canned and nowadays

it generally means delegated authentication that the person in the call center

can’t see your account information until you’ve answered a few security questions so

the internal controls also work against insider fraud against insiders helping themselves to your

money and moving it from one account to another but in this lecture and in the next one we’re

going to be concerned mainly with how do you stop external fraud against payment systems and our

goal is to understand the world payment systems and through that to get a

lens to understand cybercrime now here’s a very rapid history of banking if

you go back to the 15th or 16th century people used gold and silver coins and the merchants

would keep your assets in their vault for a fee and then after a while things evolved

so that you just hit a balance with them you give the gold merchant your 20 guineas and

he’d give you a receipt for the 20 guineas and you could go and get them back later and then

people added interest you had deposits loans mortgages various payment instruments that could

be used to finance business and to finance trade the next big innovation that came through was

paper money which was first seen by marco polo on a trip to china in the 13th century and that

gradually spread outwards from northern italy and by the time we get into the 19th century

we had a paper-based payment system with checks bills of leading all sorts of bits

of paper that flowed around the world and with them the money flowed too so

how did pepper best payments work well some countries including the uk still use czechs

although other countries have abolished them and a check is basically a written order to your

bank saying dear royal bank of scotland please pay alice a hundred pounds for my account

with you number one two three four sign bob so bob makes out this check on a check form

pulls it to alice she takes it to her bank they pay it into her account if her account is

clydesdale for example then the clydesdale will send those checks right into raw bank at the

close of day and they will all settle up now this was fine between mutually trusting parties

but the the system was problematic because of a scale and speed from the user’s point of

view it was slow it took three to ten days to to clear a check and during that time you had

a note on your account that there was a balance of an extra 100 pounds in your account but it wasn’t

cleared yet and so you might not be able to spend that money or if you were you could find yourself

with an unpaid overdraft of the czech bounced now checks sometimes did bounce either because

the the drawers account was out of funds or when the check was presented to the

drawer with their bank statement they said oh this signature is forced the whole process was

very expensive for banks and there were lots of different hacks in different countries to push

back on fraud and make the system more workable but by the time electronics came along this

was a system that was right for mechanization so how do banks send money well the simplest

case and the earliest case that was tackled was the case of sending money overseas because

that was particularly slow expensive and unsure in the old days and how things work is that

banks in scotland for example will have accounts at correspondent banks in other countries so

if you want to send your ant agatha in sydney and australia a thousand us dollars your bank

will send to national australia bank please pay australian dollars one thousand a d jones account

number xyz from our account with your number abc so this is a bit like a cheque only it’s drawn

on an account so that your bank in scotland hazard an account in australia so the technical

question now is how can you do this electronically well from the mid 18th century people invented

the telegraph samuel morrison america and charles wheatstone in britain got telegraphs going

domestically by various means and then from the 1860s we started to get international telegraph

cables thanks to lord kelvin who pioneered the thing by laying a telegraph cable across the

atlantic and the earliest users at scale among commercial firms were banks because it enabled

them to transfer money quickly and more cheaply and securely than with the old paper mechanisms

but the question then is how do you stop fraud because in an old-fashioned victorian

telegraph the messages went from one telegraph station to another where they were

copied by human operators so what was to stop a human telegraph operator intercepting a message

to the national australia bank and then making the payee one of his friends instead of your

aunt agatha well the answer was what was called a test key which was basically a manual crypto

hash now here’s a simple example but it’s not that much more simple than some of

the weakest systems that people used so what you would have is a table of um random

numbers um with uh and and here we have uh the rows are by thousands of currency units and

the columns um are by the mantissa there so if you want to authenticate 376 000 pounds

you look at the the thousands and that’s six so that’s 71 and you write down 71 you look at

the tens of thousands this is the second row that’s seven so that’s 29 so you write that

down you look at the hundreds of thousands um and um that’s three so that’s um 54 so

you write that down and you look at the millions and that zero so you write down 53

and you add them all up and this gives you 208 and you then send that along with the message now

in practice there were more numbers than this um the uh the better systems tended to have four

digit rather than two digit um random numbers in the table and the tables would be changed perhaps

once a year in order to make it more difficult for a cryptanalyst to figure out enough of

the values in the table in order to forge a telegram the system is still cryptographically

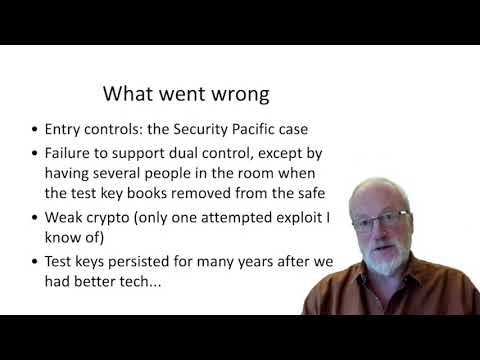

weak but it kind of worked for quite a while so what actually went wrong well um the most

famous attack on telegraphic transfer was in the 1960s the security pacific case where a bad person

at security pacific bank in in san francisco sent a telegraphic transfer for 10 million

dollars to a russian diamond company in zurich he’d arranged with them to buy 10 million dollars

worth of industrial diamonds and he sent this on a friday just before a monday that was a bank

holiday in america but not in switzerland so that he’d have time to hopefully get away and so

he basically used an internal code that was used within the bank to authorize um funds transfers

from the telegram room and the reason that this failed was that the internal procedures in the

bank didn’t support jewel control anybody could go to the telegram room and if they had the

appropriate authority which in this case was a password then the telegraph clerks would make up a

test key and send the instruction off and the only way you had jewel control in fact in the telegram

room is that there are several people in the room where the code books were and um so one one of

them would compute the code and another of them would test it but this didn’t stop internal

dishonesty now although the cryptography was weak there was only one attempted exploit that i

know of in this period where um the dictator of an african country attempted to send a 10 million

dollar wire transfer to himself and this failed because the whole country was in a one million

dollar overdraft limit but nonetheless um people realized that it was weak and they set about um

producing a replacement getting the replacement actually up and running took something like

20 years but the process started in the 1970s the replacement for the telegraphic transfer

system was put together in the 1970s by a consortium of banks who set up a jointly owned

company called swift the society for worldwide international financial telecommunications and

this was basically an early secure email system that enabled any one member bank to talk to

any other member bank and how it basically worked like this if you went into a branch of

the royal bank of scotland and sent to send a thousand us dollars to your bank agatha to to

up to your aunt agatha then the branch would send a message on its internal network to the rbs

headquarters in sight hill where they would have the room with the machinery which did swift and

swift had a set of cryptographic keys which had been exchanged with all the other banks with which

rbs did business worldwide so there would be a crypto key that had been exchanged with national

australia bank in sydney and rbs would then send a message with a message authentication code on it

so the swift regional general processor in london which would keep a log of the message that

had gone through the message would then be sent to swift’s headquarters with processing in

both belgium and the netherlands where it would be logged again and it would then be sent to the

regional general processor in australia which was down in sydney and that would then in turn send

it to the national australia bank’s headquarters where the message authentication code would be

checked so here you’ve got separate measures for integrity namely the message authentication

code and from non-repudiation namely the logging as for confidentiality that was an issue because

a number of countries at the time didn’t allow people outside government to use cryptography and

so sometimes the local link had to go in the clear key management that was done um

manually between senior bank managers because when the guy from rbs went out to

australia to set up a relationship with nab he might take a key with him in an envelope

and come back with a key from national australia bank in another envelope or they could send

it by post to each other’s domestic addresses swift also supported dual control in that while

clark a would enter transactions accountant b would check them and can change them and

then manager c would verify and release a whole batch without being able to change any

of them and so you’ve got jewel control between b and c both of whom would have to collude in

order to send a wicked message now swift at the time it was set up was owned by about 500 banks

and now it’s owned by 11 000 banks worldwide and it sends something like 125 trillion dollars

a year which is substantially more than world gdp but bear in mind when you hear such figures

that it’s the bank’s own systems that actually balance the funds and of course funds are

netted off at both ends so banks just have to settle up from time to time if their bank

accounts with each other gets out of kilter so how do you go about doing attacks on swift

well some of the sophisticated attacks have involved sending guarantees rather than cash

because if you can persuade bank a to give a guarantee to a customer of bank b then that

customer can borrow some money against the guarantee and make off with it and be long gone

by the time something is noticed whereas if you were to do an internal attack on bank a and

send money to bank b then the out of balance would be noticed within a day or two and um bank a

would be able to follow up and get the money back the second thing that we

learned with attacks on swift is that if an attacker can figure out how to

send money the hard part is in the laundry step there have been a number of cases where some

programmer at bank a put a message dishonestly into the swift message queue and then turned up

at a a bank in bangkok strasse in syria to collect the money and got promptly arrested because they

didn’t understand the difficulty of laundering money and they didn’t understand the context

and the kind of controls that you can expect to have fired up if you suddenly turn up and try

and take away 10 million dollars in a carpet bag now one of the most interesting large-scale

swift frauds that happened recently was in 2016 where the north korean government stole

81 million dollars from the bank of bangladesh they tried to steal quite a bit more and the full

story is in my book but the interesting thing here is that they managed to get away with some of

it at all and what they had done is arranged for their agents to set up in advance some

crooked deals through a casino in the philippines so that when the money arrived there there was

a chain of agents ready to launder it through further organizations that would be resistant to

law enforcement inquiries into money retrieval another aspect of attacks on swift is attacks

on confidentiality by law enforcement and intelligence agencies now before 9 11 this tended

to take the form of attacks on confidentiality on the local loop but since 9 11 the american

government basically demanded access to the entire swift message stream and after

some humming and hawing in the european parliament this was granted the americans are

particularly keen to track terrorist financing and to exclude iran so they can put on sanctions

and this has been one of the driving forces of the um behind the undermining of financial

confidentiality worldwide now we’ll come to that later when we start talking

about anti-money laundering controls the next component in the international

financial payment system is the credit card these started off in the 1950s in in new

york where dinos club and american express introduced cards so that people could

pay for restaurant meals and hotel stays and they spread slowly as an elite

product from one bank to another in the uk for example barclays introduced it

as the barclay card and it was a status thing if you’re a wealthy person to have a credit

card the other banks also introduced it and got in bed with mastercard which

was the competing global franchise this grew slowly because the difficulty in

getting any payment mechanism going is that not many people want to have your credit card

until there are lots of merchants who are accepted and yet merchants don’t want to go

to the trouble of putting acceptance machines of various kinds in all the stores until

enough of the prospective customers have got cards so that took about a generation to get going

until suddenly in the mid 1980s credit cards turned into a profitable mass market product

that’s the time when you could use a credit card in just about any store in the high street and

by then there was suddenly a race to add online authorization in the uk in order to cut the cost

of credit cards which previously had operated by imprinting a manual sales voucher which the

customer would sign a little bit like a check and we also rushed to add pins so that people could do

cash withdrawals from atms and of course the banks were happy to charge transaction fees and interest

as soon as you took cash out of your credit card what also happened then is that once credit

cards became a mass market product we started seeing credit card forgery and this was driven

initially in the far east where people figured out that you could get credit card numbers and

expiry dates from old sales vouchers or from carbon copies of virtuals that were discarded

in in rubbish bins and you could then encode these on the magnetic strips of cards and so

we started adding card verification values to stop forgery these are the three digit numbers

that you see on the signature strip on the card which aren’t embossed and so don’t end up being

embossed onto a sales voucher and the three-digit code is different on the magnetic strip so you

you can’t generate a workable magnetic strip forgery of a card just from visual inspection of

the surface so that came later in the late 1980s the third thread in the development of modern

electronic payment systems was the atm the automatic teller machine these appeared first

in britain in the late 1960s and by the time i became a student in the early 1970s um how

things worked is that we got punch cards i had four punch cards each worth 10 pounds that i

got every month with my bank statement so i could take these to a cash machine put them in put in

my pin and get a ten pound naughto and that was convenient because my living allowance for the

whole week was 10 pounds and so if i had needed anything more than that i had to get my savings

book and get money out of the deposit account now the early technology turned out to be

a bit flaky because the banks hadn’t done a particularly good job of encrypting the pin code

in the punch card and once people figured out how that worked they started forging punch cards

and getting money out of cash machines and so lloyd’s bank asked ibm for better cryptography and

ibm responded by supplying a cipher called lucifer 128-bit block cipher that had been developed by

a guy who had worked in identify friend of four systems in the 1950s the u.s national institute

of standards and technology then called for a data encryption standard and there was a big

political fight because the u.s national security agency demanded that the length of the key be

cut to 48 bits and eventually there was a long negotiation that it ended up being 56 bits long

this meant that by the 1990s it was possible for people to break theirs by exhaustive key search

and everybody figured that out back in the 1970s but this gave the banks a cycle system that was

good enough without it being good enough that it would tempt foreign governments to start using

it instead of the the stuff from crypto algae that they were using which the nsa knew how to

defeat as we discussed in the first lecture so um despite the fact that banking crypto started

off with a slightly suspect block cipher atm security really was the killer app this is

what brought cryptography into commerce and especially atm networking this is something

that i worked on for a few years in the 1980s and the goal then was to link up all the world’s

atms so that if you were an rbs customer you didn’t have to go to an rbs to get money out the

cash machine you could get out of out of bank of scotland too you could go to england get it out

of lies you could go to america and get it out of bank of america so the idea was that your cash

card would go with you wherever you wanted in the world and make your money available to you so

in order to do this we needed an international standard which operated at a number of levels

and at the level of concrete security policy the policy was that only the customer should ever

know their pin there should never be anybody in a bank who knows any pin other than their own

personal pin or who has the means to work it out and how we implemented this was with a set of

standard pin transactions using cryptographic devices called hardware security modules or hsms

and these keep pins and keys from individual bank staff and enable everything to be managed under

dual control and then you have hsms both at banks and also at the network switches at places like

visa which translate pins as transactions flow from one account to another and which also keep

track of which bank owes which other bank how much money for their customers taking money out of cash

machines so let’s have a look at how this works if i’ve got an rbs card and i go to barclays

bank atm in london i ask for 100 pounds out and i put in my pin it’s then encrypted as a hardware

security module um a a little potted chip which is um glued into the keypad and is tamper resistant

and that is then sent to the acquiring bank in this case barclays which has got an hsm at its

headquarters up in cheshire and there the pin is translated from the key that’s used to encrypted

by the atm so a key that’s used in the atm network which could be linked in those days or it could

be visa or mastercard or cirrus or whatever and then at the atm switch it’s decrypted from

the key that barclays used and re-encrypted using a key that royal bank uses and then it

flows through the network to rbs’s headquarters in site hill where they’ve got an hsm with

the key that knows how to verify my pin and can then send a message yes

or no back through the network now in theory the response messages should also be

authenticated using a message authentication code but many banks optimize this step out and

as a result we’ve occasionally seen attacks where um some bad people manage to impersonate

a whole bank and sometimes you see a bank fraud that costs tens of millions of pounds over

a weekend because somebody has managed to in comes in what else can go wrong well let’s look in the

detail about how pins are generated now this is the ibm system that ibm came up with in the early

1980s and made one of the international standards you start off with your primary account number

or pan and in this by international standards the first six digits of the bank’s identification

number so that that tells you five six tells you for example that this is a mastercard and

four one eight two tells you which bank it is and then you’ve got nine digits of account

number and one digit of a redundancy check giving you 16 digits so you then encrypt this

number using the bank’s pin key which is a 56 bit dez key or nowadays a 1 1 12 bit triple des key

which gives you a hex string output you then chop off the end the standard says that you can have

a pin of 4 to 12 digits most banks standardize on four digits one or two allow you to use five and

you then decimalize the result most of the banks all of the big banks in britain accept hsbc

decimalized by simply taking everything module 10 so b becomes 1 and d becomes 3 and so on

hsbc is different and they’ve got a custom customized decimalization table and so in this way

you’ve taken in a 16 digit primary account number and you’ve got out a four digit pin now there’s

a similar process used to generate the cvvs the three-digit check values uh on card magnetic

strips and on current signature strips but these use different keys and they also use the current

version number that’s beside the way for now so one of the problems that people then came

across is that some banks wanted to enable customers to change their pins so that they

could use more memorable pins and hopefully use the card more and generate more transaction

fees so ibm came up with a system whereby you store an offset between the original derived pin

and your chosen pin so here for example is our bank customer we’ve seen the primary account

number name is mr mk bond the balance is whatever and the pin offset starts at zero now if

mr bond decides to change his pin from 2213 that’s the derived pin that we saw in the previous

slide to 1979 say 1979 as his date of birth then you simply encode in the bank record

the the difference digit by digit mod 10 between the um the chosen pin and the derived pin

and this means that mr bond can use 1979 as a pin and the bank will verify the pin is 2213 using

its cryptography and everything works just fine but does it so here’s one of the early interesting technical

attacks that came up in 1989 there was one bank that needed to issue everybody with new account

numbers because they were replacing the core banking system with an incompatible one from

a different vendor and that was an enormous project that i worked on it took years and cost

hundreds of millions and so what the bank did was to get the hsm vendor to add a new command to the

api for the hsm to calculate the offset between a new generated pin and the customer’s chosen pin

they did this incidentally after i’d left so this wasn’t something i had an opportunity to

stop and what then what then went wrong was quite interesting because one of my successors pointed

out that any customer pin could now be revealed by calculating its offset from a known pin

because if i know how to calculate the offset between the natural pins and two accounts

i can not only calculate the offset between my old account and my new accounts i can

calculate the offset between my account and your account and so i can work out your pin

oops said the bank and they had to hurriedly contact the hsm vendor and get this new command

taken out of course the vendor hadn’t figured out that this new command would break the world

and that was telling because as time went on banks asked for more and more transactions to be

added to the hardware security modules transaction set until by the early 2000s leading models of

hsm had as many as 500 different transactions to cope with different ways in which different

banks worldwide did their cryptography then we started looking at it systematically mike

bond was in fact one of my research students who did his thesis clawing through hsn manuals

and figuring out all the ways in which they could be broken and this is one of the early

ways that we discovered you could do that when you set up the master key between two banks

or between a bank and a cash machine then what you do is you carry the master keys in two or three

parts uh you know giving them to separate couriers or posting them on different days so that you can

maintain the dual control policy if it’s an atm for example you might post one key to the branch

accountant on monday and then post the second key to the branch uh manager on on thursday

and that way you’ve got two separate people each having one key component in their separate

files and what happened with the system that visa had set up was that these components were combined

using the exclusive r function and nobody realized it at the time back in the 80s when this was

being designed but this was a serious mistake so let’s investigate why suppose you’ve got

a source hsm in a bank and a destination hsm for example in a cash machine so the

user that is the the program that manages um the bank’s atm fleet goes to the source hsm

and says generates a key component and the hsm dutifully prints out on an attached printer

in the security cage in the bank’s data center the first key component and it then returns

to the calling process that key component encrypted under a master key and you do that twice

and you then have two key components which you can post out to the guy in the bank branch and you’ve

got two encrypted key components kp1 and kp2 and to support this the visa cryptography had a

transaction which would enable you to take kp1 and kp2 both encrypted under a relevant

master key and then get them back again xor all together encrypted under that master key

and keys of this type would then be treated as atm master keys and they could be used for tasks

such as encrypting pins or were still encrypting the pin master key so that you could do offline

verification of customer pins so what goes wrong well the problem was this that a single operator

could feed in the same part twice and since kp1 xor kp1 is zero this means that you get out the

zero key encrypted under a master key and because it’s encrypted under this master key the hsm

will treat it as being a suitably authorized key under which you can then encrypt a pin master key

and in this way you could extract pins and you could extract pin master keys from the security

module so this was an attack a slightly subtle attack but once you’ve seen it it’s fairly obvious

and this had been in thousands of security modules sold by about a dozen different vendors to over

10 000 banks worldwide for a period of 20 years before the attack was observed and that’s

one of the bizarre things about the design of cryptographic protocols that they’re just

sufficiently subtle but you can have really devastating vulnerabilities in them which aren’t

at all obvious until of course someone spots them for the first time and then you can have a long

and expensive remediation process and this and other vulnerabilities led to a process whereby

pretty well all the world’s security modules had to have significant upgrades or

replacements during the early years of the 2000s many attacks were then found on hardware

security modules because of the complexity of the pin management that they

had been designed to support without anybody you know doing proper adversarial

attacks on them at the time back in the 1980s here for example is another attack where you

use the existence of the decimalization table in order to work out pins in a slightly more

indirect way than in the previous attack so here’s a typical pin verify command you put in

the primary account number you put in a trial pin this comes from somewhere perhaps from an atm

and it’s encrypted under some key or another but let’s disregard that as a detail from now and

you put in an encrypted pin master key that’s the pin master key that was used to turn this

primary account number into the pin 2 2 1 3. and you then put in the decimalization table and

for all banks in britain except hsbc that was just the decimalization table zero one two three four

five six seven eight nine abcdef translated to zero one two three four five six seven eight nine

zero one two three four five so what then happens inside the hardware security module is it takes

the primary account number it takes the encrypted pmk decrypts that under the appropriate master key

encrypts the pan gets the natural pin of 2 2 1 3 using the decimalization table and then

checks it against the trial pin 0 0 0 0 and are the two equal nor they aren’t so it outputs no so um how can you adapt this if you’ve got

access to this transaction how can you adapt this to workout pins well the thing to notice

is that the decimalization table is entered into the hardware security module unprotected

it’s in the clear and so what you can do is put in a malicious decimalization table all

zeros except for um a one opposite the input value of seven and what then happens is that when you

encrypt the pan the raw pins two to bd as before you decimalize at the natural pin is zero zero

zero zero you verify zero zero zero zero and you now get a yes and this yes tells you that

there isn’t a seven um in the natural pin and i think you can see where this is going and if you

sit down and work it out you’ll reckon that with something like typically 22 or 23 transactions

you can work out what a customer’s pin is and the interesting thing about this decimalization

table attack which makes it still relevant today is that first there’s many different variants

of it and when we first came up with that just about everybody that we told about it

thought up a new variant if they understood hsms at all because you can play with the

decimalization table you can play with the offset you can play with pin block formats you

can play with all the variables in the system but the general lesson from this is that this is

a differential attack on a private computation and nowadays people are doing all sorts

of fancy things with the cryptography on fully homomorphic encryption and private

set intersection and so on and so forth whereby you try and do some computations on

encrypted data now this is a very example a very early example of how this got done in the

1980s albeit using a hardware security module rather than fancy elliptic curve cryptography

and it went spectacularly wrong and why because people didn’t stop to think whether tweaking some

untrusted inputs of a computation could result in private inputs being leaked and this is something

that people are still not checking properly today and i predict that if we see fully homomorphic

encryption being used at scale in real applications we’re going to see attacks that are

somewhat reminiscent of this decimalization table attack on 1980s technology which was so obscure

that it was only discovered in the early 2000s so there we have some of the interesting

cryptographic stuff that went wrong with atms which led to competition between hsn vendors

and disputes over standardization and so on in the early 2000s but this doesn’t have very much to do

with what actually went wrong in terms of fraud on the street now during much of the 1980s there

wasn’t that much atm fraud there were occasional incidents of it when people worked with corrupt

bank insiders and then in the early 1990s we saw a growing tide of fraud which happened because

magnetic strip cars were easy to alter or to copy and gangs learned to do shoulder surfing

now back in those days the magnetic strip on your debit card didn’t have a cvv and

so an early attack was to stand outside a bank and look over somebody’s

shoulder as they put their pin in as they did a transaction and then if they

dropped the atm tickets on the ground you pick it up and in those days several banks

printed the full 16 digit number on the ticket so you knew the primary account number and

you’d observe the pin with your eyeball so you could then go and make a bank card and you

could steal money from that per guy that you just stood behind in the queue and there were gangs

learned to industrialize this there were a couple of guys who got a furniture van and they put

a video camera in it and um they had a motion sensor and this would then observe people at the

atm and capture a videotape with with timings on it and they would then go and empty out the waste

paper basket and pick out all the tickets with primary account numbers on them

they’d make up cards and they would loot the customers that wasn’t the only thing they

did but that was one of their tricks and there was a big law case where something like 2 000

people sued 13 banks for 2 million pounds back in phantom withdrawals in addition to implementation

bugs like putting 16 digits of the account number on the ticket which banks stopped quickly enough

there were insider attacks there was network diversion where somebody pretended online to be

a whole bank we later on found malware in atms and we had people social engineering pins for

stolen cards for example if you managed to steal someone’s purse and you found a couple of atm

cards in it what you would do if you were a bad person would be to phone them up and say hello

is that agatha jones it’s barclays bank here um security division uh tell me we’ve seen a

couple of transactions against your card with an off license in newcastle for over a hundred

pounds each time these look like suspicious transactions that you actually do them all

north of the customer thank you for calling my press was stolen i was just about to get round

to calling you and tell you to cancel the cards okay so the villain um that’s fine we’ve

stopped that one now just tell us your pin and i’ll go into the computer and i’ll stop

your card for you right and that worked often enough that it was a real issue and the banks

had to go out of the way to educate people what happened then um from the mid to late 1990s

is that fraud started to be industrialized using atm skimmers people defend invented devices that

would sit over the throat of an atm and would copy the magnetic strip as the card went in and it

then either had a little pinhole camera that would watch people entering their pin at the keyboard

or else even you’d have an overlay that sat on top of the pin pad itself and once people had

figured out how to make these they got various gangster associates around europe who would

actually act as their franchisees and would collect information from atms and this led to uh

growing problems with losses and eventually the banks in the late 1990s decided to start moving

to smart cars so they started designing standards and preparing for a rollout of smart card based

systems which started in 2004.

They also developed a number of centralized intrusion detection

systems which were capable of detecting fraud across atm networks worldwide one particularly

neat invention by a new york firm called fico signed up a number of banks um who would report

whenever they saw um a dodgy transaction at one of their atms and when that happened fico would put

that atm at the top of a hot atm list they kept a list of about the 40 baddest atms in in the world

at any one time and the thinking there was that if somebody stole a bunch of uh debit and credit

cards they typically go to an atm and try them out one after another to see if they worked and

so those banks that subscribed to fico’s service would pretty quickly find that their cards were

not working in that atm because it would rapidly go to the top of the hot atm list and therefore

the subscriber banks found that the criminals were throwing their cards away on the street rather

than actually using them to take money so there are a number of clever ideas like that but in

total they weren’t enough and eventually from 2004 the banks started rolling out the next

generation of technology the smart card the cards that are used nowadays for payments both

for debit card and credit card payments generally adhere to a standard called emv for european

mastercard and visa which developed this in the late 1990s and early 2000s these were deployed

from 2004 and unified to a certain extent the debit and credit card worlds one of the ways

in which this was rolled out was by means of what industry called a liability shift the

banks all changed their terms and conditions so that if there was a dispute if a

cardholder said i didn’t make that transaction then if the merchant wasn’t using emv

it would be charged to the merchant otherwise it would be charged to the cardholder

because the bank would say your card and pin were used therefore it must be your fault

you must be either negligent or complicit and so the banks believe that it would pay for

itself because they wouldn’t have to pay for fraud anymore the fraud costs would fall on the

card holder on the merchant so did things work out that way well it changed a lot of things

but not always in the ways that banks expected so um let’s think from the point of view

of the economics of the security of pins now with checks a fraud signature was null and

void and so if somebody gave you a check with a fraud signature on it that was your risk in other

words the forgery risk fell in the relying party but with pins banks managed to arrange things

in most countries that the risk would move to the user and they got away with arguing to

a complaining customer your card and pin were used so you were negligent or complicit

so what could possibly go wrong well this is the story of how fraud in the uk has evolved

since emv was initially introduced in 2004 and this is quite interesting so we’ll have a quick

look at it now and then discuss some of the components of it in the remainder of this lecture

and in the next lecture the first thing that you notice is that cardlock present fraud such as

the use of credit cards online to buy stuff absolutely shoots up this is the first takeaway

it rises very rapidly for a few years until 2008 when it falls slightly and then it starts

climbing again and it’s still climbing today the second is that counterfeit

card fraud went down initially but then it went up for several years

because um people figured out that once terminals were being used everywhere to collect

customer pins not just atms but also point-of-sale terminals and stores it was dead easy to use

false terminals to connect people’s card and pin data and then make up mag strip forgeries that

you used in those atms that still accepted them a number of the other types of fraud

fell or stayed at a relatively low level such as male non-receipt and id

theft which means impersonation mobile banking has started off since about 2015

and online banking since about 2010 and online banking started to climb uh from about 2013 or so

and we’ll look at these trends as we go through so as i just said car not present shot up

at once and counterfeit took off once the crews realized it’s easier to steal card and

pin details once pins are used everywhere and you could use mag strip fallback for several

years particularly overseas and what’s also interesting is that tamper resistance didn’t work

properly now in a later lecture we’ll discuss the mechanics of tamper resistance but let’s

start off by looking at the security economics suppose you’re running the merchant services

division of a bank and you can decide to pay an extra 10 pound per terminal to

make a million pin entry devices secure and thereby save the uk banking system overall 100

million a year in fraud would you do that decision well you would then say well what proportion of

the bank cards are issued by my bank and if your bank only issues eight percent of all the cards in

issue then you’re not going to bother doing that because the bank spends 10 million pounds and it

saves 8 million pounds so that’s not a business proposition are also issues within banks because

if the card divisions manager if you or the guy who goes and buys all these merchant terminals

and you’re going to spend 10 million of your budget so that your rival the current division

manager um saves 8 million on his then that’s an even less attractive proposition so there are

significant issues of governance around here and what we found for the first 10 years or so of chip and pin being deployed is that pin entry

devices were trivial to tab devices were claimed to be evaluated under the common criteria

which we’ll discuss later in the section on accreditation and evaluation and it turned out

that these were trivial to tap and the evaluations hadn’t complied with the requirements of the

common criteria and bank said no it wasn’t the problem and the common criteria brand owner gchq

just didn’t want to know and yet we found here for example with the this ingenico terminal was

the most commonly used pin entry device in the uk in the mid 2000s we found it was trivial to

tap because in the back of it there was a place where you could put some wicked electronics

and if you drilled a hole or you can see that paper clip going in that managed to

drop a contact onto the serial line which took the clear text pin from the pin pads

of the card and which got all the card data and transaction data coming back in the other

direction so with a wiretap like this you could steal enough information to make a magnetic strip

forgery of the card now all of a sudden there was concern in the industry because shell found that

it had to replace all its pin entry devices these were actually of a different make from trintek in

ireland and bad people managed to figure out how to put bad electronics in them and trintech in

fact went bust and um retired from the penentry device market so eventually the crooks taught the

bankers a lesson in governance of such systems and more lessons were to follow let’s look in

detail as a normal emv transaction you put your card in the pen entry device and the card says

hello i’m card for bank account number so and so and here’s some encrypted stuff and a

digital signature which proves that i am encrypted issued by such and such a bank and

the merchant then displays to the customer we’d like you to pay 59 pounds please

enter your pin and the customer enters one two three four or whatever it is and the

pin entry device then sends to the smart card um the pin is one two three four the amount

is 59 pounds blah blah blah various bits and pieces and the card then scratches its head

and um and says well okay the pin is right and here is an authorization cryptogram we’ll

look at the details later but basically it is a cryptogram that’s calculated using a

cryptographic keys is shared between the card and the card issuer so the merchant terminal

doesn’t know what that key is so it can’t verify it so it sends the transaction with the cryptogram

off to the issuer which then checks the cryptogram and checks whether the customer has got enough

money in their account if it’s above a certain floor limit and then sends an authorization back

to the merchant and that’s a busy period if the amount is below a certain threshold then the

transaction may be authorized offline without referring to the bank in order to minimize the

volume of transactions it has to be dealt with now in about 2010 some crooks in france discovered

that there was a flaw in this system and we started hearing reports of customers who had their

cards stolen and their cards had been used in transactions and the bank said that your pin must

have been used and the customers were insistent that it couldn’t possibly have been in one case

the customer had never used a pin with that card so what’s going on well we investigated and

we found um that if you have got some means of interrupting the transaction of intercepting the

transaction of doing a man-in-the-middle attack between the merchant terminal and the card for

example using a fake card or using an overlay card then what you can do is throw the pin on the

floor and tell the card that this is actually a chip and signature transaction instead

because these are allowed for some people and for cards for some countries and the only

difference is that a pin isn’t then sent so the card then gets the transaction thinking

it’s a chip and signature transaction and then works out a cryptogram and sends it back

to the bank and this is the kind of device that is used nowadays to do a no pin attack this is an

overlay sim you can buy these from taiwan and you can get a software development kit and they’re

about 180 microns thick and they’ve got smart card contacts on the top and at the bottom and

you can program them in java card so that you can manipulate transactions and you can use

them to attack cards that you’ve stolen or in other ways which we’ll describe later and

what then happens is that the card thinks it’s authenticated a chip and signature transaction

or the merchant terminal thinks that the customer enters the correct pin and if you then send

the transaction with the cryptogram to the bank the bank at least 10 years ago would happily

authorize the transaction because determining the manipulation means you have to look carefully

at the extra information returned by the card and by the terminal and doing that across complex

networks was a difficult thing to arrange so how could the no pin attack be blocked well

in theory you could block it at the terminal or the acquirer of the issuer but in practice

it usually has to be at the issuer because um with terminal tampering the incentives

for the acquirer are rather poor and although barclays introduced a fix in july

2010 they removed it in december 2010 we think because of too many false positives other

banks left their systems vulnerable to this and some of them even asked for one of our master

student thesis which investigated this to be taken down from the web instead and we told them what

they could do about that but it wasn’t until 2016 that british banks actually fixed this

and to this day we come across cases of british tourists in china who’ve had their cars stolen

where this kind of attack appears to have been carried out and the real problem here is that

the emv spec is now far too complex you’ve got a hundred plus vendors 20 000 banks millions of

merchants and everyone passes the buck and it’s really really difficult to change anything

once the system has scaled up to that size and what we’ve also found is that the api

attacks we were talking about earlier on the hsms keep on coming back so for example vs

visa defined a new hsm transaction to support emv where the idea was that you would be able to

send a cryptographic key from one hsm to another as a text string followed by a key and amazingly

they allowed the text to be variable length and this led to a simple attack where you

could encrypt text followed by 0 0 and then text followed by 0.01 and so on in order to work

out what the first byte of the key was and then by varying the length of the text you could get out

the key one byte at a time and this vulnerability turned up in all the compliant hsms worldwide

because visa had specialized and specified it and so basically what was happening is that as soon as

the hsm industry removed the api vulnerabilities the banks put them back because the governance

of the whole system was basically shot now here’s another example of how emv went wrong atms and

random numbers i said i’d look in detail about how the authentication request cryptogram is done

and here it is the terminal sends a random number this is known in the spec as the unpredictable

number we will just call it n here so the card along with the date d and the amount x and one

or two other things such as the currency code and the arqc is a mac computed using a key that

the card has and the bank also knows on nd and x so what happens if i can predict n for d if i

know what unpredictable number a given terminal will use tomorrow and if i get access

to your card i can pre-compute an arqc for that given amount and on that particular date and how did we figure this out well

we got a complaint from a guy in malta who had gone on holiday to majorca and he ate

a meal in a rather dodgy perhaps mafia-owned restaurant and the following day he found four atm

transactions on his account that he uh didn’t make and so he complained to hsbc and malta his uh his

bank and they said well our system is secure and your card and pin were used so it’s your fault

and we’re debiting you so he demanded the logs of the disputed transactions and he came to

us and this is what we found looking at the logs that the unpredictable number which you

can see in the right hand column ended up being a 17-bit constant followed by a 15-bit

counter that cycled every three minutes so we put together a test one of my postdocs

had some fun wiring up a bank card um with a clock chip and a microcontroller and some memory

so we could take fine-grained timing measurements of bank transactions that we did around atms in

the uk and we found that a bit over 40 percent of atms in the uk are also simply using counters

as unpredictable numbers and the reason for this we figured out is that in the emv spec the

testing for the unpredictable number simply says that the tester has to draw three numbers from

the device and check that they’re all different now if you’re a programmer in a hurry then using

a counter is a fast way of passing that test so how does this work out in practice well

the pre-play attack that we found in practice around europe was something that we first came

across in 2014.

Um a british sailor went into a bar in las ramblas in barcelona the big fancy

streets in downtown and he paid 33 dollars for two drinks 33 euros for two drinks and he woke

up at six in the morning with a sore head because his drink had been spiked and he then got on a

plane to paris and he then checked his account and he found that 33 000 euros had been taken from

his account at lloyds in 10 payments of 3 300. so why does a sailor have 33 000 euros while he was

working out of aberdeen on the rigs that’s why and so he went to lloyds and lloyd said your

car and pin card and pin were used so it’s your fault and so he went to a law firm and the

law firm came to us and we got the logs and we found that ten transactions had been made an hour

apart for 3 300 euros each from the same terminal but through three different banks and

with different terminal characteristics so this was clear evidence of technical tampering

and so lloyd’s basically grumbled a bit and gave him his money back and the lesson here is

that emv lacks a trustworthy user interface and so what a bad person can do is that they can

monkey with the software in an emv terminal and get it to display the wrong amount of money

to you so that you think you’re authorizing a 30-pound transaction when you actually authorize

uh 3000 pounds or that you’re actually authorizing 10 transactions when you think you’re actually

authorizing one and this can also be done by sticking one of these overlays onto the customer’s

card before you stick it in your terminal and we’ve seen a pattern of activity whereby these

kind of scams are done in red light districts all the way around europe we’ve seen them in poland

we’ve seen them in the baltic states and we have even seen them in the uk in bournemouth the

council had a dispute with a lap dancing club the spearmint rhino and the councillor came to us and

they said that multiple customers had complained of excessive car charges they’d go in and buy a

drink for the young lady for 50 quid and they’d be charged 5 000 and sometimes they woke up with

a sore head in the morning and if they complained to the bank the club just said well he was with

two girls all night and that’s what we charge the banks and the police weren’t

interested but the council was worried uh because of course if you’ve got an

establishment that starts anesthetizing people um or they’ve got full stomachs and without

medical assistance then sooner or later someone’s going to end up dead and you’ve got

a murder in your hands and so the counselor got the bournemouth echo to speak to us and they

wrote about the pre-play attack and about 20 more victims contacted the councillor and as a result

the club’s license was restricted for six months and still the police weren’t interested and we

did what we could to try and um contact the local authorities but nope um that’s not something

that they wanted to do in bournemouth or also for that matter in poland and this is actually

rather concerning now when you think about it the cards that you’ve got in your pocket um

have perhaps got a total overdraft ability several thousand pounds quite apart from any

money that you’ve got there and the banks will very often give you extra unsolicited overdrafts

so they can charge you more money for them so if you go into a red light district

establishment with three or four bank cards in your wallet it’s as if you’re going in

there with five or ten thousand pounds in cash now would you go into such an establishment carrying

five or ten thousand in actual banknotes well hey that’s one of the downsides of card payment

that if things go wrong they can go very wrong