We” ve obtained a couple of even more

information today from Geithner and the Obama management regarding their plan for saving the financial institutions. I figured that this is a.

good time to analyze examine they” re proposingSuggesting and see.

, if we can come to any type of final thoughts.. So, just to simplify the.

Perhaps it” s Citibank. Let ‘ s say they have one large bad. That was the initial book.

worth for the property. And they had the ability to do that. And clearly these financial institutions have.

a number of properties, so I” m oversimplifying it.But I believe it ‘

ll get you. the core of the problem. They did that by– obviously a.

great deal of them leveraged a lot extra– however let” s state they. made use of $40 of equity.

And then they borrowed. And currently of course, this.

And it ‘ s the equity tranche. on these home loans. And I urge you to watch the.

videos on collateralized financial debt obligations, and home loan.

backed protections. And also the entire thing, all.

of the videos that we did on Paulson” s original. bailout strategy. Since I speak about all the.

liquidity issues there. The lower line is that several of.

these financial debts are coming due for these banks. So they need to unload these.

properties to get cash. And the entire issue here is,.

Worth$ 100, dollars?’these banks

don Put on t want desire. If they unloaded for 50 cents.

You” d be with this fact. And you owe $60. There” s absolutely nothing left for the

.

bank. So simply to set the framework. There” s a substantial reward why the.

bank doesn” t want to offer this asset for anything less.

than 60 cents on the buck. The trouble is, the most that.

any person” s going to pay for it now is not even the.

60 cents on the buck. Individuals are just willing to pay–.

I” ve read records and it depends on what possession you” re. This is what banks want. Greater than 60 cents.

And in this case, it” s. $100, so $60. My understanding is until now, for.

one of the most part, without any government treatment, the.

There” s this disconnect. The financial institution” s like

, well I ‘ m not.

Every day there” s much more. It ‘ s even hard to get good.

documents on what supports these car loans. A lot of these were.

these NINJA finances. No revenue, no task loans. Or these liar car loans, or mentioned.

income financings, where people can simply load out with anything.

they want. And there” s all this fraud.So people are marking down a great deal.

of risk right into these assets. Essentially, the market.

isn” t operating. The purchaser” s readiness to pay. is a lot slower than the vendor” s willingness to offer. And absolutely nothing takes place. Therefore, these harmful properties are,.

you could say, blocking the system. Due to the fact that the banks, I won” t say. that they can ‘ t sell them. It ‘ s simply they ‘ re not prepared. to offer them. Because if they were

ready. to sell them at the market price– whether or not you concur.

with this market rate– the banks will certainly be bankrupt. So the government all along.

has been attempting to come up with different models of exactly how.

can we somehow obtain these assets off the banks’ ‘ equilibrium. sheets without creating the financial institutions to obtain financially troubled? And the original version of TARP.

1 is that the federal government will basically buy these.

possessions for, who understands, 70 cents on the dollar. And in that truth, if you.

acquired those properties for 70 cents on the dollar,.

after that those possessions, you” d have $70 here.The financial institution would owe $60. And there would certainly still be a.

little bit left of equity. There would be $10 left. Yet the important thing is that.

the financial institution would be able to pay off its responsibilities, stay.

liquid, and afterwards be around for a better day or a far better.

economic climate, where it can expand the equity base again by.

buying every one of that. And everybody understood.

that the tarpaulin was a scams on some degree. If the because when you do that.

market rate really is 30 cents on the buck, and.

you” re paying 70 cents. Let me state, if this TARP 1. And the government pays 70.

The government” s overpaying. In this instance, the federal government.

would be creating a $40 check to the proprietors of this company.In this situation

, the.

shareholders. And these are the extremely same.

individuals the management and the original capitalists in a whole lot.

of these companies. These are the very exact same people.

who obtained us into this mess. And why need to we be rewording.

them billions of bucks of checks to basically.

simply bail them out. Why don” t you just. take them right into receivership and all that? And I” ll do various other. video clips on that. The brand-new version that has.

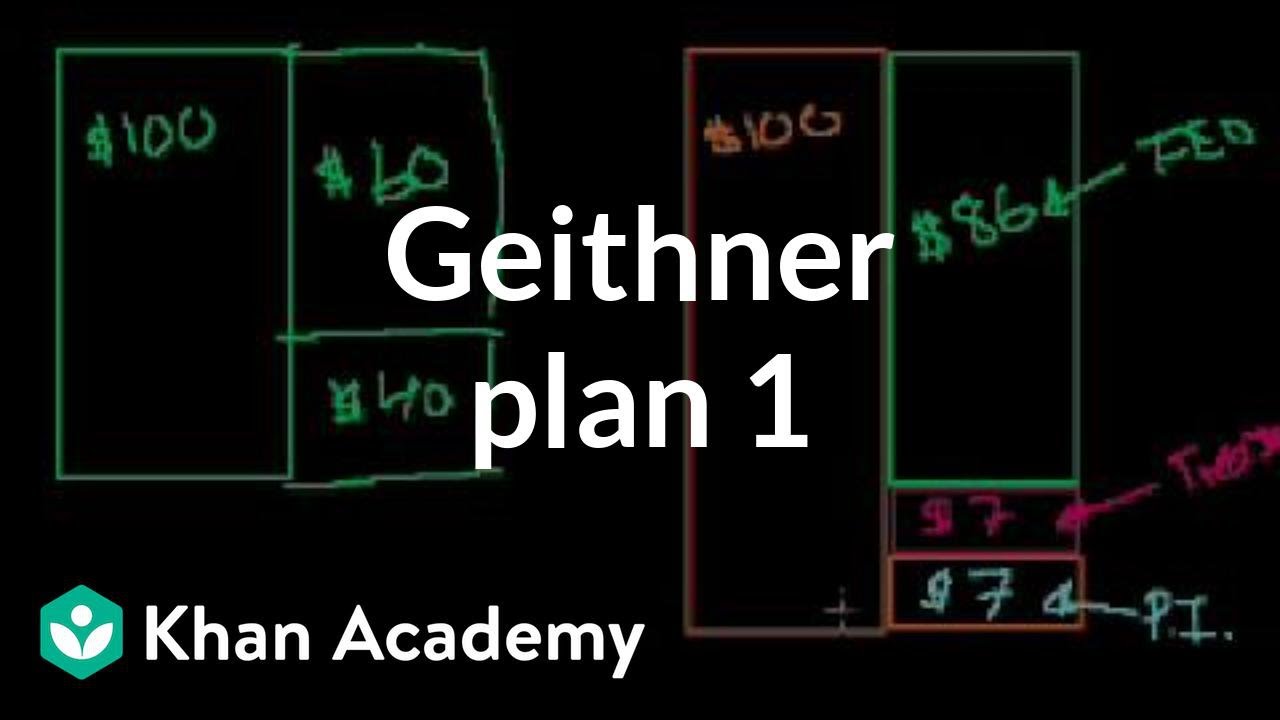

happened– and allow me scroll down a little– is, and.

let me attract the original scenario. You have this product.

right here that was initially paid for $100.

They borrowed $60 to.

buy them. And after that they have.

$ 40 of equity. The new strategy is, the.

government” s stating, you ‘ re right, taxpayer.

We as a government, we ‘ re not. in’a position to decide what things deserve

. We ‘ re not hedge fund supervisors. or’common fund supervisors. We ‘ re simply bureaucrats. And you ‘ re.

We would probably just finish. up overpaying for points. Since these individuals are clever. And if they ‘ re not happy to. pay even more than 30 cents, and we ‘

re paying 70, we ‘ re. overpaying, and it ‘ s just a large aid from the taxpayer. So the brand-new Geithner strategy is.

saying, hi we” re mosting likely to companion with the exclusive.

investors. And the means they” re suggesting.

they do that, is that allow” s state a private investor– and. these are numbers that I ‘ ve read in some

of the. paper reports, and the numbers might change with time.

due to the fact that they do have a tendency to.But exclusive financiers will.

add, say, $7. This is from personal.

capitalists. The Treasury will certainly add.

another– allow me make an additional box– will type of match.

that investment by the exclusive financiers. So the Treasury will certainly add.

one more $7. And afterwards the Fed is going.

to provide the balance. The Fed– allow” s see, if you.

Let me draw a box right here. It ‘ s going to look something. That ‘ s$ 86.

from the Fed. And of program, this entity,.

when it ‘ s originally taken advantage of, is going to be. remaining on$ 100 money.

That ‘ s its assets. Well I ‘ m saying it.

Fed lent $86. This is a finance.

The Treasury made a straight. equity financial investment of$ 7.

And exclusive capitalists make a. straight investment of$ 7.

And after that this entity can then. go and purchase these possessions

. And what the government– at. least my analysis of it is– is

that the private investors are. going to establish the price.So the exclusive financiers are. going to say, you understand what? I assume that this thing. right here deserves, I put on ‘ t understand, I assume it ‘ s worth 70 cents. on the buck. And allow ‘ s state that they.

are the winning quote. They are individuals happy to. pay one of the most.

Since that ‘ s my reading. Is that there will.

That in that instance– let ‘ s say. After that they ‘ ll have. After that we ‘ ll have the

toxicHazardous

Sal, that ‘ s crazy. And you ‘ re.

situations, they obviously wouldn ‘ t pay. Actually, as a result of that, allow.

me not make$ 100 the number. Allow ‘ s claim that they.

pay$ 60 for it. Due to the fact that, remember, the financial institutions. weren ‘ t even willing to get rid of

them for much less than$ 60.

So for this to also work,. somebody ‘ s mosting likely to have to pay at the very least$ 60 for’this thing.

So allow ‘ s say they. pay $60 for it.

And afterwards they obtain the asset.

And they” re mosting likely to. have$ 40 left over. So they have toxic asset, and. They ‘ re going to have actually $40 left over, due to the fact that they only.

paid $60 for the protection. The means I set it up. They probably designed. this thing so there isn ‘ t any kind of money left over. Let ‘ s simply use these. numbers for the purpose of convenience.

Now, you may say,. The private capitalists

, they made.

Currently they ‘ re prepared to pay.

And there ‘ s a pair. of answers here.

I indicate, the kind of ignorant response. Or if these things end. The rest of the loss is.

This financing by the Federal. Book is a non-recourse car loan.

lending institution– which remains in this case the Fed– can” t go after.

the equity holders.All the lender can

do. is take the property.

So if this possession deserves.

absolutely nothing, the Fed, all it can do is just take the property, and.

basically it” s going to obtain absolutely nothing back for its funding. So in this scenario, the.

private investor would certainly get all of the benefit. If this thing that they paid $60.

for ends up being worth, let” s state it finishes

up being.’worth– I ‘ ll draw it’down right here due to the fact that it ‘ s all mosting likely to the. equity holder– if that possession they paid $60 for, it if it finishes.

up deserving $80 then that additional$ 20 of value is.

going to be divided by the Treasury and

the personal. capitalist. So allow me give you.

What would the balance. They pay$ 60 currently.

All of an unexpected that. possession is worth $80.

This is an excellent circumstance,. an upside circumstance.

Remember, we had actually$ 40 left over. in cash, just based on the means I had actually originally established it up. You owe $86 to the Fed, the.

Federal Get, which is officially separate from the.

Treasury, different entity. And afterwards the equity is split.

$86 So you have$ 34 of equity? And it ‘ s going to be split. 50-50, so it ‘ s going

to be$ 17 for the private investorFinancier

And it went to $17. It” s obtained a big return.

on financial investment. This is the positive.

situation. And after that the negative scenario,.

where allow” s claim that initial financial investment actually.

winds up being worth $30. Remember they had $40 of money.

in the way I establish it up.Now all of an unexpected the Federal.

Book, you had a car loan from the Fed for $86. Now your possessions deserve less.

than your liabilities. Your equity is wiped.

out, right? So in this bad scenario, the.

exclusive capitalist invested $7, and it mosted likely to zero. So this doesn” t actually look.

like that bad of a circumstance. That in an up situation, you go from.

$ 7 to $17, And in a negative situation, you go from $7.

to zero bucks. And in fact, this could be.

amplified a lot a lot more, relying on exactly how these.

points exercise. However this still begs the.

question, if a capitalist actually thinks that these things.

deserve 30 cents, and that there” s no opportunity that.

they” re worth greater than 60 cents, although they.

overmuch can take part in the upside,.

about the disadvantage, which I believe in of.

itself is wrong.That the government shouldn ‘ t be.

supporting hedge funds and other personal capitalists. Yet if they actually assumed that.

the value was closer to 30 than to 60, then the concern.

is, why would they participate in any way? I mean, if you recognize you” re. mosting likely to lose money, you shouldn” t do it to start with. And I realize I” ve. run out of time.’I ‘ m going to cover that.

in the next video. And to some level,.

the next video clip you could locate unpleasant. See you soon.

They did that by– undoubtedly a.

lot of them leveraged much a lotA lot more but yet” s say state.’these banks

don Put on t want desire. The bank” s like

, well I ‘ m not. It ‘ s just they ‘ re not ready. And they” re going to.