hello there every person in this video clip we will certainly find out about xero promo code bonds and how to price them in Python prior to we begin let” s assess the plans we will certainly utilize they consist of matplotlib and numpy allow” s begin by specifying what an absolutely no promo code bond is’ ‘ A no voucher bond is a financial debt security that pays no interest zero voucher bonds are cost a price cut to their par value at the no voucher bonds maturation day the par value is paid to the financial debt owner the difference between the purchase price of a zero voucher bond and the share value stands for the Financier” s return right here we have the formula for a no bond bond in the numerator we have the par worth and in the we have one plus the required discount rate for repaired by the market split by the frequency in this case the frequency can be annual in that case the F would amount to one semiannually if F would certainly amount to two regular monthly or quarterly then we boosted it to the regularity increased by the time to expiry quoted over years allow” s look at no voucher on Bonds in the marketplace a preferred kind of zero voucher bonds or treasury strips a treasury bond coupon repayments and major repayment additionally recognized as the par worth are divided to develop a strip strips are backed by the full confidence and credit rating of the United States federal government which implies that the danger of default is extremely reduced business can also issue absolutely no discount coupon bonds for instance Apple Inc offers 6 year no coupon Bonds in Europe back in 2019 nonetheless there is substantially more danger in absolutely no discount coupon bonds issued by firms due to the fact that companies are more probable to skip on debt contrasted to countries like the USA currently that we have an understanding of no voucher bonds let” s produce a python feature to rate zero discount coupon bonds the way we do it is we start calling def what we” re mosting likely to produce python feature then we require to call our python feature I” ll call it no pricer then we require to specify the parameters that require to be input to price the bond and we have actually the criteria provided here we need to define the par worth the price cut price called for by the market the number of years until expiration or when the bond ends and lastly the compounding duration following thing I” m going to do I need to inspect the type of intensifying duration I desire the person utilizing this function to key in whether their annual semi-annual or quarterly intensifying even monthly the means we will do this is I” m going to start an if elif declaration I” m mosting likely to claim if the compound duration is input after that I” m also mosting likely to use the dot lower feature in situation they take advantage of at the beginning and if it equates to is on annual then I” m going to have a composite worth equal to one so that when we separate it’by the frequency it ‘ s mosting likely to be yearly so we

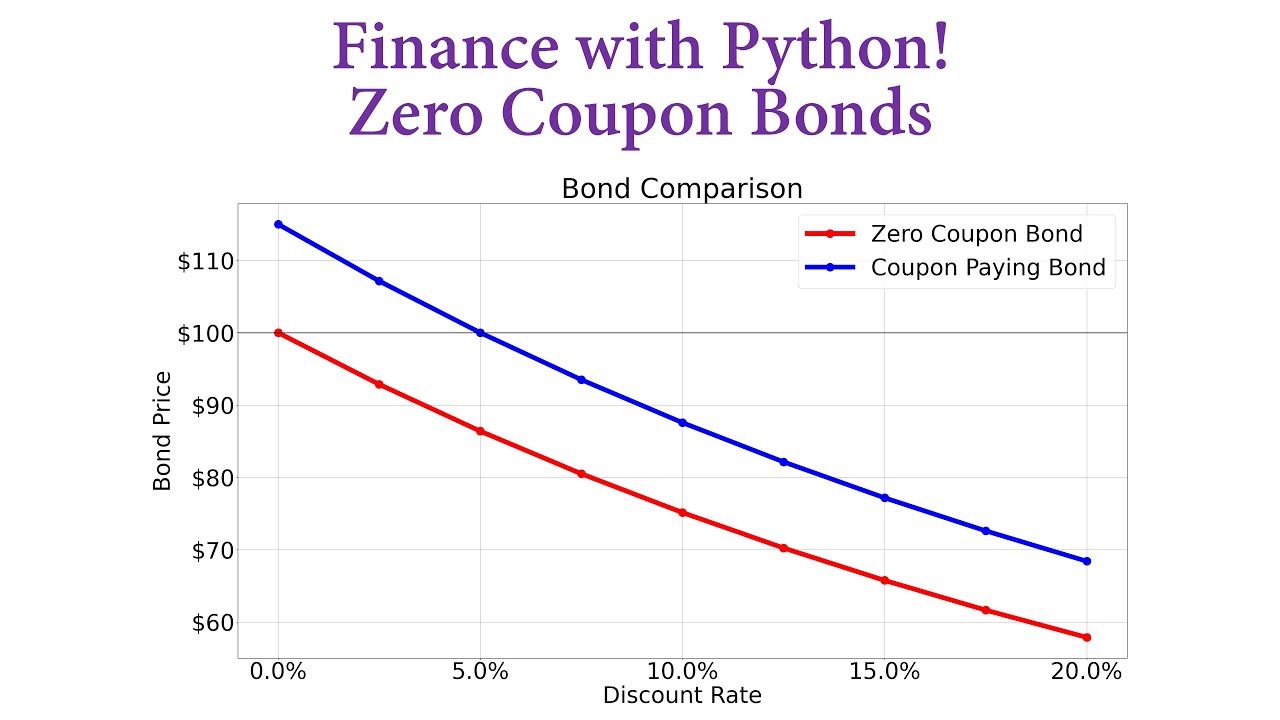

separate it by 1. And I ‘ m going to do this for a few other durations likewise then we have our alif statement indicating it is to examine if the individual enters monthly or semiannually quarterly then we have the equivalent values like 2 4 and 12 respectively for each of the following what I want to do is I wish to actually calculate the worth of the bond I” m mosting likely to create a variable called Z Bond then like the formula I” m going to take the par value and divide it by the price cut price and we require to take the discount rate we need to separate it by the compound value after that we require to boost the denominator by the compound value increased by the variety of years when we do this we use two asterisks to increase it then lastly we wish to return the value of the bond itself so I require to return Z Bond specify worth we have our feature currently produced allow” s see if we deciphered what I have here is a promo code Bond example so we” re an analyst we ‘ re screening with prices is zero coupon Bond that grows in ten years with a par value of one hundred dollars the Market” s discount rate is 5 percent and the profile manager desires us to compute the bond value making use of semi-annual intensifying what I” m mosting likely to do is I ‘ m mosting likely to interest our feature the absolutely no Bond pricer after that I” m going to go all the parameters enter in below the initial is mosting likely to be the par value so we understand that it is 100 then we need to enter the price cut rate which is mosting likely to be five percent in this situation I need to kind in 0.05 after that we need to put in the number of years expiration 10 after that finally I have to go into the substance frequency in this in instance we desire it as semi-annual and below we have the value of our bond this is the approximated worth so if we wish to get this presently a bond that matures in one decade with a par value of 100 that is intensified semiannually and has a five percent price cut price the present bond cost will certainly most likely be sixty one dollars and 3 cents for this absolutely no promo code bond allow” s consider an extremely essential variable when considering the no coupon bond what is price sensitivity sensitivity similar to other bonds when rate of interest rates rise the worth of absolutely no coupon bonds falls due to the fact that investors currently demand higher payouts because zero discount coupon bonds do not make acting voucher settlements they are most sensitive to rate of interest modification to which they are extra delicate has rate of interest altered as promo code paid bonds below we have a bond pricer for a routine voucher paid bond we will certainly not go with this I will do a separate video clip that outlines just how to a coupon paid bond in the meantime but we have our function right here to price a coupon to pay Bond what I” m mosting likely to do next is I” m going to use checklist comprehension what I want to do is I wish to price absolutely no coupon bonds at different rate of interest let me type that out then examine the code to describe what going on right here we have our feature to print your very own promo code bonds and the only variable I transform is the discount rate I keep the par worth the exact same the variety of years to maturity the very same and the substance frequency the exact same at annual and we can see if the discount rate increases the worth of our bond lowers what I wish to do is I” m mosting likely to wait in a list I” ll then call it the Z bond listing what I additionally desire to do is I intend to run this exact same checklist understanding for our voucher pay Bond keep all other variables constant other than the price cut price and we can see that for our coupon Peg Bond the only distinction is we have the real discount coupon repayment yet let” s plot it out and take an appearance and we can see that the worth of the absolutely no discount coupon bond what is this red line is considerably less than the voucher Bank pays bond that makes sense since the promo code pays Bond also gives you voucher payments in this instance it” s at’5 percent so that ‘ s 5 bucks a year you get these coupon bonds over those 3 years which dramatically has even more value than a no voucher bond that just pays the primary one hundred dollars at the maturity date of the bond thanks all for viewing I hope this video clip was handy I have actually included extra recommendations you can check Investopedia does a very excellent task in recap of monetary principles you can likewise really feel totally free to such as And subscribe you can additionally get in touch with me on LinkedIn Twitter GitHub and odyssey thanks everybody for watching and pleased coding