PART 2: WHAT” S WRONG WITH THE TEXTBOOK MULTIPLIER

DESIGN? We” ve seen the two main concepts that the general

public have concerning the means financial institutions function. Both of them are incorrect. That” s not as well unexpected,

nevertheless, unlike the Favorable Money group many people wear” t spend their time consuming regarding just how banks function. And banking is intricate, which implies that the majority of people offer up trying to recognize it. However what regarding business economics or financing pupils? Many of these graduates and students have a somewhat far better understanding of banking. They obtain taught concerning something called the ” money multiplier ‘. The cash multiplier story says that financial institutions actually create much of the cash in the economy.Here ‘ s how the

tale goes: A guy walks right into a bank and deposits his wage of ₤ 1000 in money. Currently the financial institution knows that, generally, the consumer won” t require the whole of his ₤ 1000 returned simultaneously. He” s possibly mosting likely to spend a bit of his wage each day throughout the month. The financial institution assumes that much of the cash transferred is ” idle ‘ or spare and won” t be required on any kind of specific day. It maintains back a small ” get

‘ of say 10% of the cash transferred with it (in this instance ₤ 100), and offers out the other ₤ 900.

to someone that requires a funding. So the borrower takes this ₤ 900 and invests.

it at a neighborhood auto dealership. The car supplier doesn” t want to keep that.

much money in its office, so it takes the cash back to another bank.Now the bank once more becomes aware that it can utilize. the bulk of the cash to make an additional loan. It maintains back 10% – ₤ 90– and offer out.

the other ₤ 810 to make an additional car loan. Whoever obtains the ₤ 810 invests it, and it.

comes back to among the banks again. Whichever bank receives it then keeps back 10% i.e.

₤ 81, and makes a brand-new financing of ₤ 729. This procedure of relending continues, with.

the very same money being lent over and over once again, yet with 10% of the cash being placed in the.

get every time. Note that each of the clients who paid.

cash into the bank still thinks that their money exists, in the bank. The numbers on.

Also though there is still only ₤ 1000 in cash moving about, the sum total of every person” s. bank account balances has actually been increasing, and so has the complete amount of debt.Supposedly this process continues, till after.

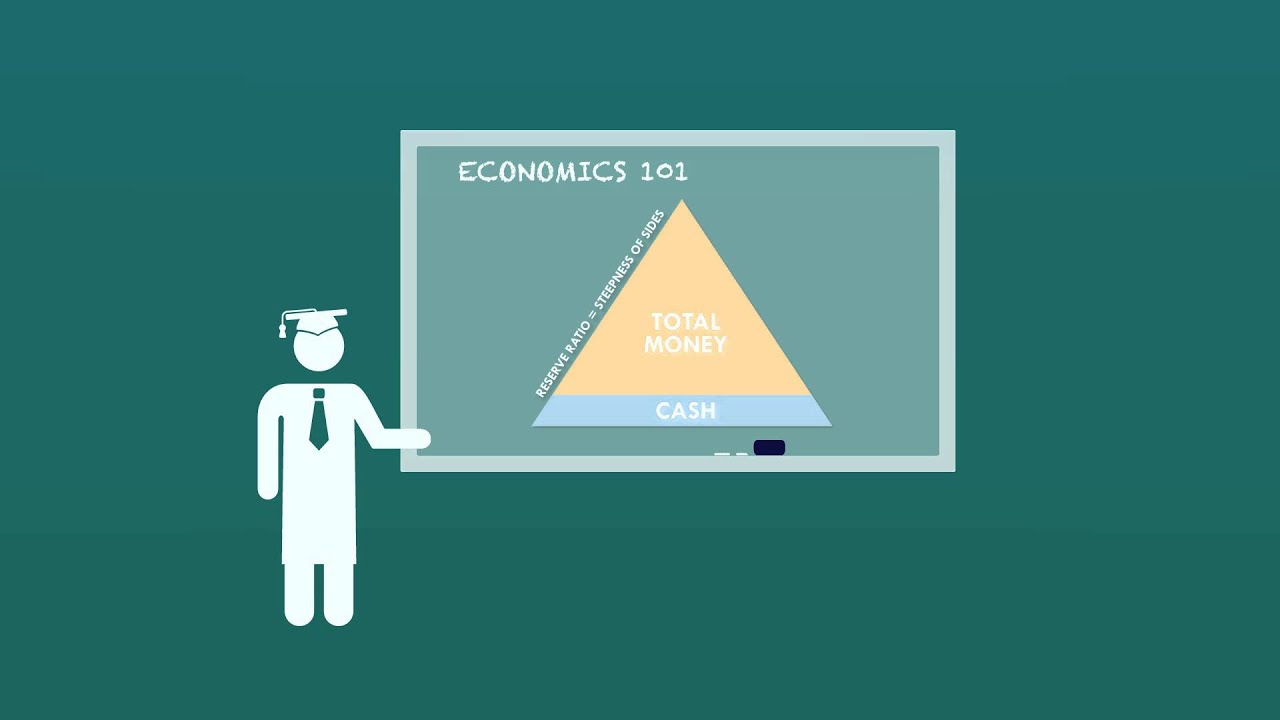

The version states that if the reserve ratio– that ‘ s the percentage of consumers ‘ money that. It ‘ s a unreliable and obsolete means of describing just how the banking. Banks in the UK sanctuary ‘ t functioned like this for years.

The reality that this pyramid design is still. This is not exactly how it actually functions, as we ‘ ll see. It implies that the central financial institution.

of customers ‘ cash that banks have to maintain in reserve- or the amount of ‘ base cash ‘.– cash money– at the bottom of the pyramid.For example, if ‘the Bank of England

sets a. lawful reserve ratio– and this book ratio

is 10 %, then the total money supply.

can expand to 10 times the amount of cash in the economic climate. After that increases, if the Financial institution of England. the get proportion to 20 %, after that the money supply can just expand to 5 times the quantity of cash money. in the economy. If the book ratio was dropped to 5 %, after that the money supply would expand to. 20 times the amount of money in the economic situation. The Financial Institution of England might change. just how much cash there remained in the economic climate in the initial area. , if it printed one more ₤ 1000.. and put that into the economic climate, and the get proportion is still 10%, then the theory claims

that. the cash supply will raise by an overall of ₤ 10,000, after the financial institutions have undergone. the process of repetitively re-lending that money.This procedure is called changing. the amount of ‘ base money ‘ in the economic climate. The most considerable

implication of this. design is that the Financial institution of ‘England, or’ the Federal Book or European Central Financial Institution,. has total control over just how much money there really remains in the economy. If they transform the. size of the base–

by pumping more ‘ base money ‘ right into the system– then the overall. quantity of cash need to increase.If they change the get ratio, after that the pitch of the.

Ultimately, the reserve proportion quits the cash supply expanding. At some point we reach the top of the money and the pyramid supply stops.

expanding. There ‘ s absolutely no possibility that the money supply can get

out of control. There ‘ s simply one small trouble. Practically every little thing. concerning this summary of banking is wrong. As a matter of fact, Professor Charles Goodhart, of the.

London College of Business economics and an expert to the Bank of England for over three decades,.

It could be forgivable for textbooks to be.

27 years, later on college trainees are still learning a description. of banking that is completely unreliable. This is a huge trouble. If these trainees then. take place to end up being economists and experts to the government, and they put on ‘ t even actually. understand how cash works

, after that our economy might end up in a genuine mess. Oh wait … it already is! Currently, I need to explain that these video clips. do apply to the UK, and we haven ‘ t had time to validate specifically how things work in the. U.S.A. and Europe. For those of you in the US, a paper published in 1992 refers to’a. book still made use of in colleges today– and specifies that “the multiplier design … is. at ideal a misleading and insufficient model, and at

worst a completely mis-specified design ‘. Right here ‘ s the lower line when it comes

to. the ‘ cash multiplier ‘: 1. There ‘ s no book ratio in the UK any longer,.

and there hasn ‘ t been for a very long time.

2.

And the Bank of England absolutely doesn ‘ t. have control over just how much cash there remains in the economy in total.It ‘ s not simply economics graduates who have.

the incorrect info. Even people operating in the Treasury still think it works’according. to the textbook.

We ‘ ve had letters from the Treasury saying things like this: In connection with the point about the control. of’money, it is the Bank of England alone which has control over the financial base.

Financial institution of England. Commercial financial institutions are liable for prolonging credit scores to people and businesses. It ‘ s like permitting design.

pupils who wear ‘ t understand gravity to construct high-rises.

They get educated regarding something called the ” money multiplier ‘. Also though there is still only ₤ 1000 in cash money moving around, the amount overall of every person” s. financial institution account balances has actually been increasing, and so has the complete amount of debt.Supposedly this process proceeds, up until after. The version says that if the get ratio– that ‘ s the percent of customers ‘ money that. Banks in the UK haven ‘ t worked like this for years. There ‘ s definitely no possibility that the cash supply can obtain

out of control.