So simply to obtain us back up to

speed where I left off in the last video clip, we have a bank

remaining on a possession that it perhaps originally

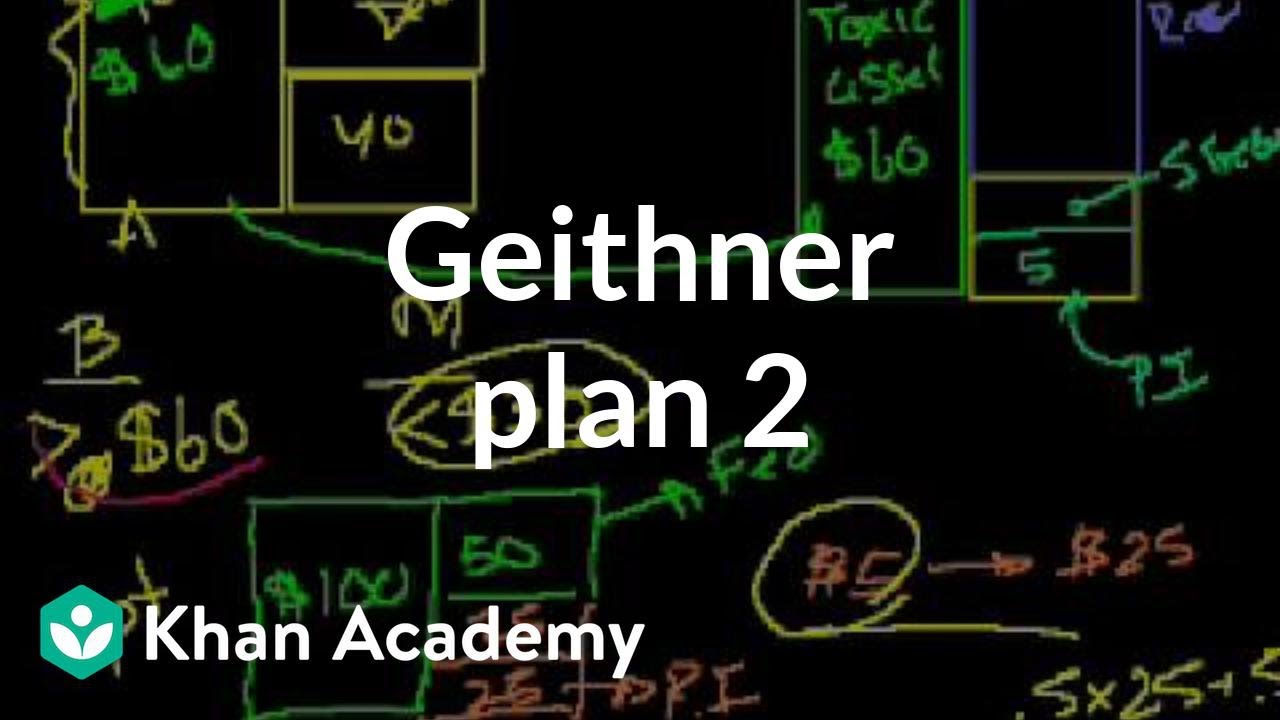

$40 of equity. That ‘ s when they paid for it. And they had$ 40 of equity.

And the financial institution is insolvent. Allow me draw their equity. Allow” s claim that you have

–.

so you have $5. from an exclusive investor. This is an evaluation of.

the last video. You have $5 from the Treasury. These are both the.

equity financiers. And afterwards you have $50 borrowed.

from the Fed. And I” m doing this a little.

bit in different ways, so the numbers pair up precisely.

with what they” re mosting likely to pay for the asset.So you have$ 50

. Let me see. If that” s $10,$ 50 would certainly. be something that looks something like that. You have $50 that you borrow from the Federal Reserve. Therefore, this entity will.

have $60 below. When it obtains taken advantage of. We” ll do that in eco-friendly. And what they can currently.

do, is they can consider that $60 to the financial institutions. Essentially paying a cost that.

the banks agree to get rid of the assets for. And after that the financial institutions are going.

to provide the properties. So currently the bank has $60 of money.

that it can use to keep its responsibilities fluid. And now this entity right.

here has a hazardous property, we can call it. And I addressed it in the last.

video clip, you understand, why is the financier doing this? Because they share disproportionately in the upside.They paid$ 60

for this point. And equally as a genuine fast evaluation,.

if this point winds up deserving– let” s say it. winds up deserving $100.

After that they owe$ 50 to the.’ Federal Get. That ‘ s this funding right here.

To the Fed. And then they split the equity. with the Treasury.

Exactly how much equity? There ‘ s an overall of $50. of equity left.

$5, and it went to $25. That” s awesome. 5 times your cash.

What ‘ s their down case? Their down case is– allow ‘ s. say that harmful possession actually is worth$ 30.

It ‘ s vital, since. Let ‘ s claim that this. This is pessimistic.

So allow ‘ s claim these possessions. wind up deserving $30.

You have this$ 50. lending from the Fed.

And you have no equity.

leftover. And the Fed basically. is left writing off its finance.

The private financier, since. there ‘ s no equity, is going

to be left with zero.So you went from$ 5 to absolutely no. This is still a pretty.

good risk/reward. Depending upon just how you weight.

these likelihoods. But a great deal of people, if you.

thought that there” s an equal chance of this and this. occurring, you would take this wager. If you had a 50% opportunity of.

making five times your cash, and only a 50% opportunity of.

losing your money, the expected worth right here is, it would.

be 0.5 times 25 plus 0.5 times zero. It would be a $12.

expected value.So I would

pay $5 for something.

that has a $12 anticipated value. That” s a terrific return. You ‘ re making 140%.

on your cash. You don” t see returns.

like that every day. Unfortunately, the possibility.

of these 2 points happening aren” t similarly likely. Since certainly today, the.

market” s ready to only pay $30 for these points. The market, if they assumed that.

there was any type of possibility that these points deserve more than.

$ 60, any opportunity, they” d be trading at greater than $30. Provided where the present.

market is, prior to government intervention, plainly no-one.

assumes that there” s an actually likelihood of them.

There” s a much greater.

And you might weight.

the likelihoods. And if you make this possibility.

high sufficient family member to this one, after that of.

program the anticipated value is still going to be.

much less than $5. You” re still anticipated.

to lose cash. Therefore you may state, well,.

who would do that? Despite The Fact That Paul Krugman is out.

there stating, you know, this is one of those heads.

I win, tails you lose kind of circumstances. And that holds true. In the positive circumstance, the.

personal financier makes the bulk of the cash, together with.

the Treasury. With the Fed simply obtaining an extremely.

low interest rate back on this money. While in the unfavorable scenario,.

many of the hit is going to be taken by the Federal.

Get with their financing, and then the Treasury.

who” s an equity investor alongside them.So that is among these.

I” d state, that also if that,.

still wouldn” t desire to spend it, if this is the.

most likely scenario. So the question is, that.

is going to do this? And this is what I stated.

in the last video, could be unpleasant. The obvious point is that the.

financial institutions might intend to get it from themselves. So let me revise every little thing. Since this is an essential.

And frankly, I put on” t. understand exactly how you can stop this from occurring. If this variation of Geithner” s. plan finishes up passing.

annual report. They paid $100 for.

these possessions. They owe $60. All responsibilities, down payments,.

whatever. And originally they have.

$ 40 in equity. What the bank does is it takes.

some additional money, and they might elevate equity,.

or for all we understand they can raise cash. I mean, the federal government is giving.

This isn” t fiction. What you do is allow” s

sayClaim And this is occurring.

fundings to these major financial institutions, to Citibank and Bank.

And they” ll get $7 of. Now what the financial institution does is, they.

They can call it

whatever. they want.They might place it in a hedge.

fund to do this. I suggest, banks are terrific. Unique objective entities.

happen regularly. And there” s nothing to quit a. financial institution from placing this $7 right into one more entity. One more unique objective.

entity. Where the financial institution essentially.

has the equity. And this cash money went to that. And after that taking this $7.

and using this to join the plan. In this new Geithner plan. The financial institution takes that $7 that.

they essentially could have just borrowed from.

the federal government. Gets involved in the plan as.

the exclusive financier. And I” ll put that in quotes. And they could place a lot of.

layers below and obfuscate it. Or perhaps get among their bush.

fund clients to do it, by providing excellent terms.

on something else. I mean, there” s a million. and one ways you might set this up. And that” s why I assume it ‘ s. difficult to enforce laws around, or legislate.

to avoid it.So they do that there. The Treasury will certainly take part.

side-by-side as an equity investor. And then they” ll borrow $86.

from the Federal Get. That” s from the Treasury. And now the bank is essentially the personal capitalist.

They ‘ re regulating.

this entity right here. They ‘ re regulating entities. that control that entity.

It doesn ‘ t matter. They essentially established the.

price for which this entity is going to pay for. its very own properties. They can pay$ 100.

for this thing. Although everyone understands that. these things are worth no place near$ 100. They pay$ 100 for this. Take it off their. annual report. And’after that they ‘ re sitting. with $100 money.

And this is sitting there.

with a harmful asset.And why would a bank do this? Well, think of it.

In this fact, before any of. It had this entire point.

right here, it had exposure to. And for all we understand, they” re. only worth$ 30.

The financial institution never wanted. to approve that truth.

While in this fact,. the bank only has $7 exposure to it. So also if this thing winds up. exploding,’who ‘ s going to take’the loss? The financial institution ‘ s just mosting likely to. take a$ 7 loss right here. And after that the remainder of the loss.

is mosting likely to most likely to the taxpayer; the Treasury and.

the Federal Book. So this is an awesome.

situation. When, since in this truth. there was a hit, if this was worth $30 the bank would. have to take a$ 70 hit.

While in this truth, if this. poisonous asset now is only worth $30, the financial institution” s only going.

to take a$ 7 hit.And the bank is

going. to remain solvent.

This financial investment right here. is going to be erased.

However still, the bank. obtained $100 in money. My concern is, and truthfully.

given that there” s absolutely nothing to prevent it, it” s almost a.

self-fulfilling prophecy that” s going to occur. You have this big inquiry.

mark, why would certainly an exclusive capitalist ever take part.

in this? Also if the federal government is kind.

of providing you even more of the advantage than the downside. You wouldn” t participate

in. If you thought that the drawback situation, it.

is more most likely. But you would join.

it, if you were the real vendor of the safety. If you are the vendor, since.

of the safety and security, you are Citibank, you” re going from. 100 %direct exposure to only 7% direct exposure, and you” re going.

to be remaining solvent.But the web effect

of this is. that the Treasury and the Federal Book, they got.$ 100 for something.

Or I think, if you take. out the$ 7, they essentially obtained $93. Due to the fact that they had to spend$ 7. to make this point happen.

But they obtained$ 100. So they got $93 for something. that ‘ s truly worth$ 30’. So the distinction, the $63, it.

essentially would be a check that” s being composed from the.

U.S.Taxpayer to these banks. It would be a$ 630.

To me, this would certainly be kind.

of the biggest takeoff of capitalism. And it would be a sad day. It would frankly just make the.

AIG perks look insignificant. The right response is, you take.

that $630 billion, make the financial institutions erase their.

shareholders, and afterwards you recapitalize the financial institutions.

with the cash. And after that you begin, rather than.

creating the $63 or the $630 billion check directly to.

the management and the shareholders who obtained us into.

the mess, you essentially recapitalize the new banks. And I” ve created a paper.

about that, and there” s a brand-new bank plan. And distribute the shares.

to the American people. And you get the exact same result.

without this hugely adverse consequence of providing a massive.

riches transfer to the similar people that.

got us in the mess. Anyhow, I really hope people kind of.

jump on this story, due to the fact that it” s got me quite troubled.Anyway, see you.

That ‘ s when they paid for it. It ‘ s crucial, because. And there” s nothing to stop a. financial institution from placing this $7 into one more entity. And that” s why I believe it ‘ s. difficult to pass about, or pass.

The bank ‘ s simply going to.